Cash Collection Cycle: Meaning, Delays, and How to Improve

The cash collection cycle depends on what happens after invoices are sent. Manual processes and rule-based AR automation struggle to keep up with real customer responses. This guide explains why cycles stretch and how Lunos, one of the best AI coworkers on the market, improves collections without adding headcount

Quick Summary

The cash collection cycle depends on what happens after invoices are sent. Manual processes and rule-based AR automation struggle to keep up with real customer responses. This guide explains why cycles stretch and how Lunos, one of the best AI coworkers on the market, improves collections without adding headcount.

How Much Are Small Breaks in Transmission Costing You?

Late payments rarely announce themselves as a crisis. Over time, those small delays compound. The cash collection cycle stretches because the process stopped keeping up with reality. Finance teams feel the pressure long before leadership sees the numbers change.

This article breaks the cash collection cycle down in practical terms. We’ll look at what it really is, why it deteriorates as companies grow, and how teams actually improve it without burning out their AR function or damaging customer relationships.

Why Listen to Us

At Lunos, we spend our time inside post-invoice collections with finance teams. Our team combines extensive knowledge of AI and software with over 50 years of experience. We know where typical AR automation helps and where it quietly stops being useful. That perspective shapes how we think about the cash collection cycle. It is a living system made up of conversations, follow-ups, exceptions, and human judgment.

What Is the Cash Collection Cycle?

The cash collection cycle is the period between issuing an invoice and receiving the corresponding cash. It is a workflow that lives across people, systems, and client engagements.

At a high level, the cycle includes:

- Sending the invoice

- Guaranteeing the customer receives and acknowledges it

- Managing reminders and follow-ups

- Handling customer replies, questions, and disputes

- Tracking payment promises and expected dates

- Receiving, reconciling, and recording payments

A long cash collection cycle commonly suggests:

- Inconsistent outreach

- Missed or late feedback

- Poor visibility into what customers have actually said

What Actually Influences the Cash Collection Cycle?

Several real-world factors determine how long it takes for cash to arrive. These factors exist whether teams acknowledge them or not:

- Consistency of Follow-Ups: Customers are more likely to pay on time when follow-ups happen reliably. Gaps create room for invoices to slip down priority lists.

- Speed of Response: When customers reply with questions or delays, the clock resets. Fast responses keep momentum. Slow ones stretch the cycle.

- Clarity of Intent Tracking: A promise to pay “next week” is valuable only if someone tracks it and follows up at the right moment.

- Handling of Exceptions: Disputes, partial payments, and internal approval delays need different treatment. Treating everything the same slows resolution.

- Visibility Across Systems: When payment data, email threads, and notes live in separate tools, no one sees the full picture. Follow-ups become reactive instead of planned.

Why Do Cash Collection Cycles Break as Companies Scale?

Most cash collection cycles break down for a simple reason: the early processes were never built to withstand the wild pace of growth. When volumes are low, AR relies on memory and grit.

Collectors remember who promised what, track invoices by hand, and squeeze follow-ups into the cracks of their day. But as the business grows, that old map just doesn’t cover the territory anymore.

When a key AR team member leaves, their context leaves with them. The replacement starts with partial knowledge, and customers feel the inconsistency.

Leadership pressure often increases at the same time. CFOs want tighter control over cash. Controllers want cleaner, closed cycles. AR teams are asked to do more with the same tools.

As the business grows, several things happen at once:

- Invoice volume increases faster than headcount

- More customer replies arrive every day

- More exceptions appear

- Coordination across sales and finance becomes harder

Common failure points at scale include:

- Follow-ups delayed because collectors are overloaded

- Payment promises forgotten when inboxes fill up

- Disputes sitting unresolved because they were not flagged clearly

- Forecasts based on outdated or incomplete information

How Do Most Teams Try to Improve the Cash Collection Cycle?

When cash collection slows, teams usually respond in two predictable ways:

1. Manual Fixes

These help temporarily but increase the workload. They do not scale:

- Sending more reminder emails

- Creating more detailed spreadsheets

- Adding calendar reminders

- Holding more internal check-ins

2. Traditional AR Automation

These tools reduce some manual sending. However, they often stall at customer replies. Many teams then turn to automation tools designed to:

- Schedule reminder emails

- Standardize outreach cadences

- Trigger escalations after set delays

When a customer responds with:

- “We’ll pay next Friday”

- “We’re waiting on approval”

- “There’s an issue with this invoice”

Automation usually stops. A human must read the reply, interpret it, update systems, and decide the next step. The promise of automation fades into partial relief. The core limitation is that most tools automate actions.

What Actually Shortens the Cash Collection Cycle for Good?

Apart from sending messages faster, sustainable improvement comes from managing conversations well. Teams that consistently shorten their cash collection cycle do a few things differently:

- They respond quickly to customer replies

- They track intent, not just due dates

- They remember and act on payment promises

- They surface exceptions early instead of letting them stall

- They sustain consistency even under volume pressure

How Can Finance Teams Improve the Cash Collection Cycle in Practice?

Improving the cash collection cycle starts with tightening the workflow after invoices are sent.

If these foundations are shaky, not even the slickest AI can bail you out. But when you get them right, a tool like Lunos becomes your force multiplier. The teams that truly rein in the cash collection cycle focus on three things:

1. Process Fixes that Reduce Friction After the Invoice is Sent

Most delays in the cash collection cycle happen after invoicing. Improving the process means removing ambiguity in what happens next. When collectors know what should happen next, fewer invoices drift simply because no one was sure how to proceed.

High-performing finance teams typically standardize a few core practices:

- Clear Follow-Up Ownership: Every invoice has a clear owner at every stage. There is no ambiguity about responsibility.

- Documented Follow-Up Expectations: Follow-ups are not assigned to individual judgment alone. Teams define what “timely” means for first reminders, responses to replies, and missed payment promises.

- Explicit Handling of Common Scenarios: Payment promises, approval delays, and disputes each have a defined path. This prevents every reply from becoming a one-off decision.

- Early Exception Surfacing: Issues are flagged as soon as they appear, rather than waiting for due dates to pass. This keeps accounts from stalling silently.

2. Metrics that Reflect Reality, not Only Results

Many teams measure the cash collection cycle solely with lagging indicators. While data points like days sales outstanding (DSO) are important, they do not explain why the cycle is lengthening.

Teams that actively improve their cycle track leading indicators alongside outcomes.

These metrics handle friction early:

- Response Time to Customer Replies: How quickly the team acknowledges and responds to inbound messages.

- Promise-to-pay Adherence: How often customers follow through on stated payment dates, and how quickly missed promises are addressed.

- Exception Resolution Time: How long disputes or questions remain open before being resolved or escalated.

- Follow-Up Consistency: Whether reminders and check-ins happen as planned or are frequently delayed.

The challenge is that most teams lack a single place to track these indicators without manual reporting (which is where a tool like Lunos comes in handy—more on that later).

3. Team Workflows that Scale Without Adding Headcount

The cash collection cycle breaks because the workload grows faster than capacity.

To improve cycle time without adding headcount, finance leaders focus on workflow design. Follow-ups happen on time because the system supports them, not because individuals push harder.

When workflows are designed this way, consistency improves naturally:

- Separate Routine Work from Judgment Work: Not every follow-up requires manual decision processes. Teams identify which actions are repetitive and which sincerely need expertise.

- Centralize Context: Customer communication, promises, and notes live in one place. Collectors do not waste time switching tools to reconstruct history.

- Cut Back on Reliance on Memory: Systems, not individuals, track commitments and future moves. This protects the cycle from turnover and overload.

- Protect Focus Time: Collectors are shielded from constant inbox triage so they can focus on exceptions and high-risk accounts.

When Do Traditional Improvements Reach Their Limit?

Process fixes, better metrics, and improved workflows can greatly shorten the cash collection cycle. But they have a ceiling.

Recognizing this limit is not a failure. It is a sign that the organization has outgrown operational refinement alone and needs a different kind of leverage.

As volume grows, one challenge remains constant: someone still has to read, understand, and act on customer replies. This work simply becomes the new bottleneck.

At this stage, teams commonly experience a choice:

- Add headcount to preserve uniformity

- Accept slower collections as a cost of growth

- Or find a way to handle judgment-heavy work at scale

This is where traditional AR automation begins to fall short. It can schedule and send, but it cannot consistently interpret intent, track nuanced promises, or adapt follow-ups the way a human does.

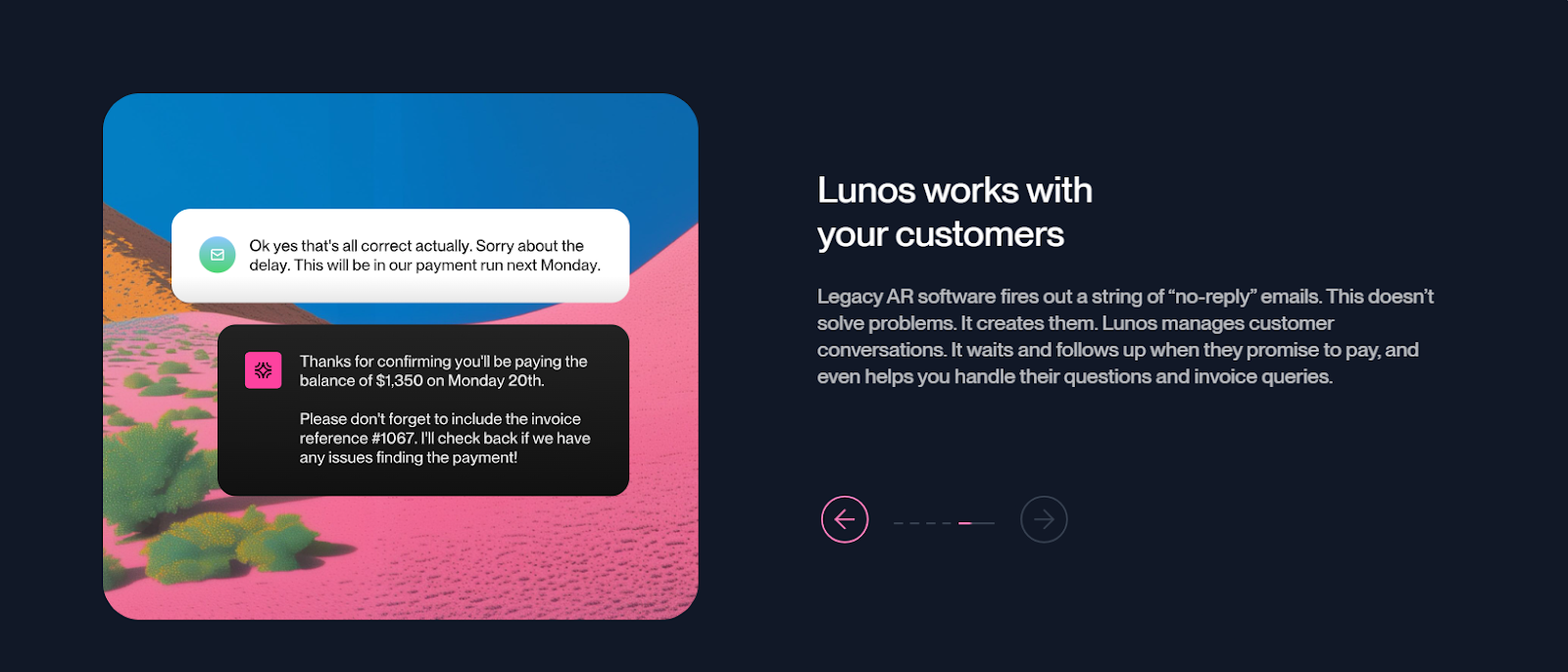

How Do You Move from AR Automation to an AI Coworker?

Traditional AR automation focuses on scheduling and sending reminders. An AI coworker handles the work that happens between reminders. It reads replies, understands intent, tracks commitments, adjusts follow-ups, and escalates exceptions when needed.

That’s why Lunos is miles ahead of rule-based automation tools, handling the real work that happens between reminders.

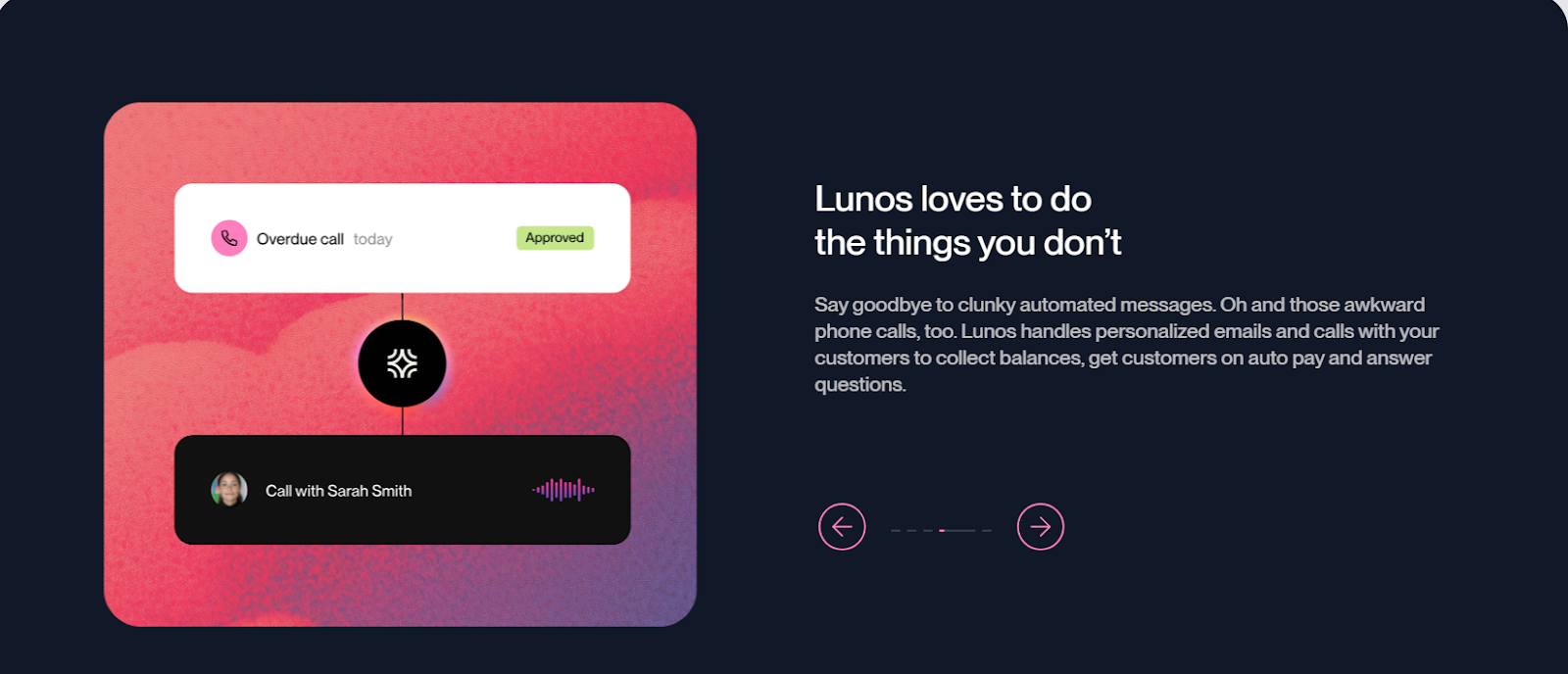

Instead of rigid rules, Lunos manages two-way conversations. It connects to your ERP, CRM, email, and payment systems and works within your existing workflow.

Crucially, teams stay in control through three autonomy modes. This structure addresses the common fear around AI by making control explicit and visible:

- Monitor: Lunos observes activity and provides summaries

- Suggest: Lunos recommends the next steps for approval

- Act: Lunos handles follow-ups independently while logging everything

How Does Lunos Improve the Cash Collection Cycle in Practice?

In day-to-day use, improving the cash collection cycle with Lunos looks different from how it does with traditional tools.

Here's how it typically plays out:

- An invoice is automatically issued and tracked.

- Lunos monitors customer communication related to that invoice.

- When a customer replies, Lunos reads and understands the message.

- If a payment promise is made, Lunos records it and schedules the appropriate follow-up.

- If the promise is missed, the follow-up happens automatically.

- If a dispute or question arises, it's routed to the right person immediately.

The cash collection cycle tightens because nothing is forgotten and nothing depends on memory. Since every engagement is logged, finance teams gain real-time visibility into customer intent, clear forecasts based on actual promises, fewer dropped follow-ups, and less manual inbox management.

Lunos's Insights Lab reinforces this visibility with real-time access to key collection metrics. Teams can track AR aging summaries, collections over time, average days overdue when paid, and average days to paid without pulling manual reports or reconciling data across systems.

How Do Teams Know When to Move Beyond Automation?

Most teams reach a clear inflection point. At this stage, the issue is no longer effort. It’s capacity. The work itself needs help.

This is where an AI teammate actually pulls its weight, as the extra set of hands that never misses a detail and never needs a breather.

Some of the signs include:

- AR teams feeling constantly behind despite automation

- Leadership questioning why DSO remains high

- Forecasts feeling unreliable or too optimistic

- Frustration with tools that automate sending but not thinking

Improve Cash Collection Cycle Without Burning out Your Team With Lunos

The cash collection cycle reflects how well a business manages real payment conversations at scale. Improving it means showing up consistently, understanding customer intent, and following through every time. Manual processes break under volume and traditional automation helps, but only to a point. Beyond that, teams need support that behaves more like a teammate than a scheduler.

Lunos acts as the tireless teammate who wrangles the repetitive work, tracks every promise, and frees you up to focus on strategy and the tough calls. Cash comes in faster, your team finds its footing, and the cycle stays tight even as your business blazes new trails.

If your cash collection cycle keeps stretching despite your best efforts, it may be time to stop adding rules and start delegating the work itself. Start your demo today.