Average Days Delinquent (ADD): How To Calculate + Improve

Average Days Delinquent (ADD) focuses solely on late payments, showing the average number of days past due for unpaid invoices. That clarity helps teams pinpoint real problems and take action. In this guide, we’ll explain what average days delinquent is and how to calculate it. We’ll also share 7 practical ways to reduce it, including using an AI assistant to handle collections conversations and ease the workload on finance teams.

Quick Summary

Average Days Delinquent (ADD) focuses solely on late payments, showing the average number of days past due for unpaid invoices. That clarity helps teams pinpoint real problems and take action.

In this guide, we’ll explain what average days delinquent is and how to calculate it. We’ll also share 7 practical ways to reduce it, including using an AI assistant to handle collections conversations and ease the workload on finance teams.

What Is Average Days Delinquent (ADD)?

Average days delinquent is an important part of the cash collection cycle that measures how many days, on average, your customers take to pay their invoices after the due date. That's it. It's not measuring the time to payment from the invoice date. That's DSO (days sales outstanding).

ADD only cares about the delinquency period.

If your payment terms are Net 30 and a customer pays on day 30, that payment does not factor into your ADD. But if they pay on day 50? Those 20 days past due are what ADD captures.

This metric gives you a much clearer picture of your collections problem than DSO alone. You might have a DSO of 45 days, which sounds reasonable. But if your ADD is 30 days, that means most of your receivables are seriously overdue.

Your on-time payers are just bringing down the average.

Why Trust Us

At Lunos, we spent years watching finance teams struggle with the same frustrating bottleneck: accounts receivable isn't really a payment problem. It's a communication problem.

And that communication costs companies millions.

We’ve worked with finance teams handling anywhere from 500 to 50,000 invoices per month and understand firsthand what actually reduces delinquency at scale.

So when we talk collection success, we know what we’re talking about.

Why ADD Matters More Than You Think

We’ve worked with finance teams that obsess over DSO while overlooking ADD. That's like a doctor monitoring your overall health but ignoring your blood pressure. Sure, the big picture matters, but the specific metrics tell you where the real problems are.

Here's why ADD deserves your attention:

- It reveals cash flow impact in real time.

- It's an early warning system for bad debt.

- It measures your collection's effectiveness.

- It exposes customer payment behavior patterns.

How to Calculate Average Days Delinquent

Calculating ADD requires a few steps, but once you understand the logic, it's straightforward. You're figuring out 3 things:

- Your overall collection speed (DSO)

- Your best-case collection speed if everyone paid on time (BPDSO)

- The difference between them

What's a "Good" ADD?

Here's the honest answer: it depends.

In a perfect world, your ADD would be zero. Everyone pays on time. You never chase anyone. And cash flows smoothly into your bank account. But we don't live in that world, especially in B2B commerce, where payment delays often stem from complex approval processes, budget cycles, and genuine disputes.

A low ADD (under 10 days) generally indicates healthy collections and good customer payment behavior. Your team is staying on top of overdue accounts, and customers are responsive to follow-ups.

A moderate ADD (10-25 days) is common in B2B, especially when dealing with larger enterprise customers with longer internal payment processes. It's not ideal, but it's manageable if you're actively working to improve it.

A high ADD (over 25 days) indicates significant issues. Among other things, it can mean:

- Your collections process isn't working

- Your customers are struggling financially

- You're extending credit to the wrong accounts

This level of delinquency directly impacts your cash flow and increases the risk of bad debt.

Industry matters too. Manufacturing and distribution companies typically see higher ADD than SaaS businesses due to longer payment cycles and more complex billing. Compare your ADD to industry benchmarks, but more importantly, compare it to your own historical performance. If your ADD is trending upward, that's your signal to act.

7 Strategies to Reduce Average Days Delinquent

Knowing your ADD is useful. Reducing it improves your cash flow and makes your finance team's life easier. Here are seven strategies that work, based on what we've seen help real finance teams reduce their delinquency rates.

1. Tighten Your Credit Assessment Process

Many ADD issues begin before you even send an invoice. If you're extending credit to customers who can't or won't pay on time, you're building delinquency into your AR from day one.

Before offering credit terms, do your homework. Check credit reports, request trade references, and review payment history if they're an existing customer. For new customers with limited credit history, consider requiring a deposit or offering shorter payment terms (Net 15 instead of Net 30) until they demonstrate reliability.

And here's something many finance teams miss: review your existing customers regularly. Just because someone paid on time two years ago doesn't mean their financial situation is the same today. Annual credit reviews help you spot trouble before it becomes a collections problem.

2. Make Your Invoices Crystal Clear

Confusing invoices lead to payment delays. I've seen invoices held up for weeks because the customer couldn't determine which purchase order to match it to, or the payment instructions were buried in fine print.

Your invoices should be dead simple. Clear line items, obvious due dates, prominent payment terms, and multiple payment options right there on the invoice. If customers have to hunt for information or reach out to ask questions, you've already added days to your ADD.

Consider including the specific payment method instructions, not just "pay by ACH" but the actual routing numbers and account details. The easier you make it to pay, the faster people will pay.

3. Set Up Automated Payment Reminders

Manual follow-up is where most collection processes fall apart. Your team is busy, inboxes are overflowing, and it's easy for follow-ups to slip through the cracks, especially when you're dealing with hundreds of invoices.

Automated reminders ensure every customer gets consistent communication at the right time. Send a friendly reminder a few days before the due date, another on the due date, and escalating reminders at regular intervals after that (3 days past due, 7 days past due, 15 days past due, and so on).

The key is consistency. When customers know they'll hear from you at specific intervals, they're more likely to prioritize your invoices. And automated systems don't forget or get too busy to follow up.

4. Personalize Your Collections Approach by Customer Segment

Not all late payments are the same. Some customers are chronically late because they don't prioritize your invoices. Others experience occasional rough patches due to cash-flow issues. Some are your best customers who accidentally overlooked an invoice.

Treating everyone the same is inefficient and can damage important relationships. Segment your customers based on payment history, account value, and relationship importance. Then adjust your approach:

- Chronic late payers: Shorter payment terms, stricter follow-up, or requiring payment upfront

- Occasional late payers: Standard reminders with a more collaborative tone

- Key accounts with payment issues: Personal outreach to understand the problem and work out a payment plan

This kind of personalization requires actually knowing your customers, which is nearly impossible to do manually at scale. That's where smart tools (we'll get to this) make a real difference.

5. Offer Early Payment Incentives

Sometimes the problem isn't that customers can't pay. It's that they have no reason to prioritize your invoice over the dozens of others sitting in their accounts payable (AP) queue.

Early payment discounts (e.g., 2/10 Net 30, meaning 2% off if paid within 10 days) provide customers with a financial incentive to pay faster. For many businesses, sacrificing 2% on invoices is worth it to receive cash 20+ days earlier.

You can also offer other incentives: preferred service levels for customers who consistently pay on time, or payment plans that make it easier for customers to manage their cash flow while still getting you paid.

6. Resolve Disputes Quickly

One of the biggest ADD killers is disputed invoices. A customer questions a charge, the invoice gets put on hold, emails go back and forth for weeks, and suddenly you're 45 days past due on what should have been a simple payment.

Create a clear dispute resolution process. When a customer raises an issue, acknowledge it immediately, assign ownership to a team member, and set a timeline for resolution. The faster you handle disputes, the faster invoices get paid.

This also requires actually seeing disputes when they happen. If customer emails are scattered across different inboxes or buried in threads your team hasn't read yet, you're already behind.

7. Deploy an AI Coworker to Handle Collections Conversations

This is where things get interesting, and where the biggest ADD reduction happens for most teams.

All the strategies above are good. But here's the reality: they're incredibly time-consuming to execute manually, especially at scale. Your finance team spends hours every week sending follow-ups, reading customer responses, tracking payment promises, figuring out who needs a reminder, and who needs a different approach.

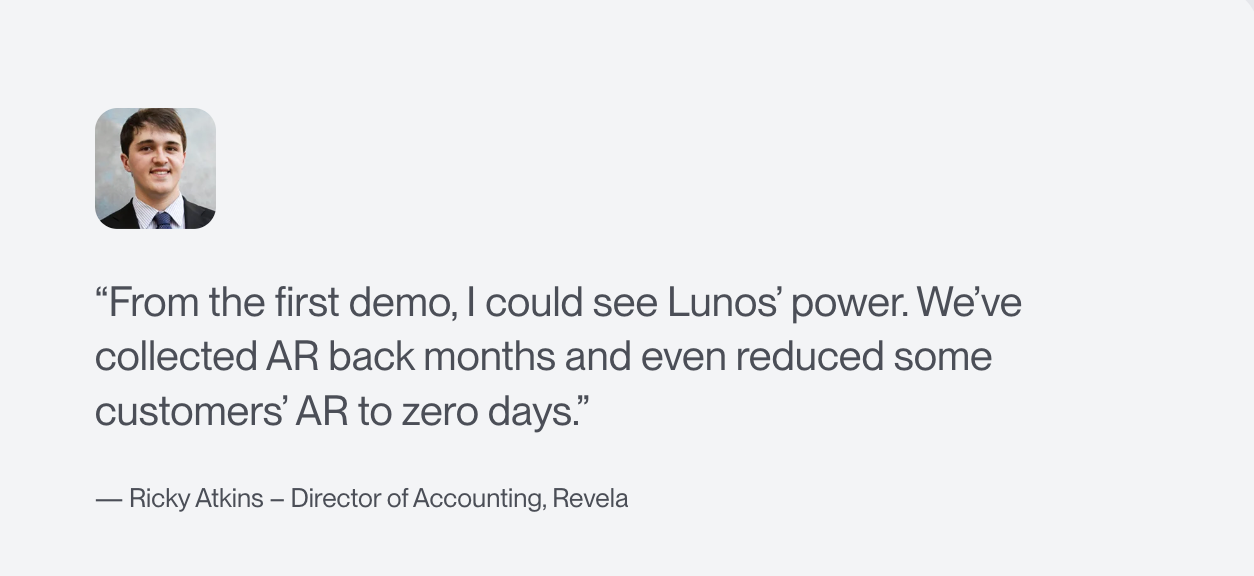

That's exactly what we built Lunos to solve.

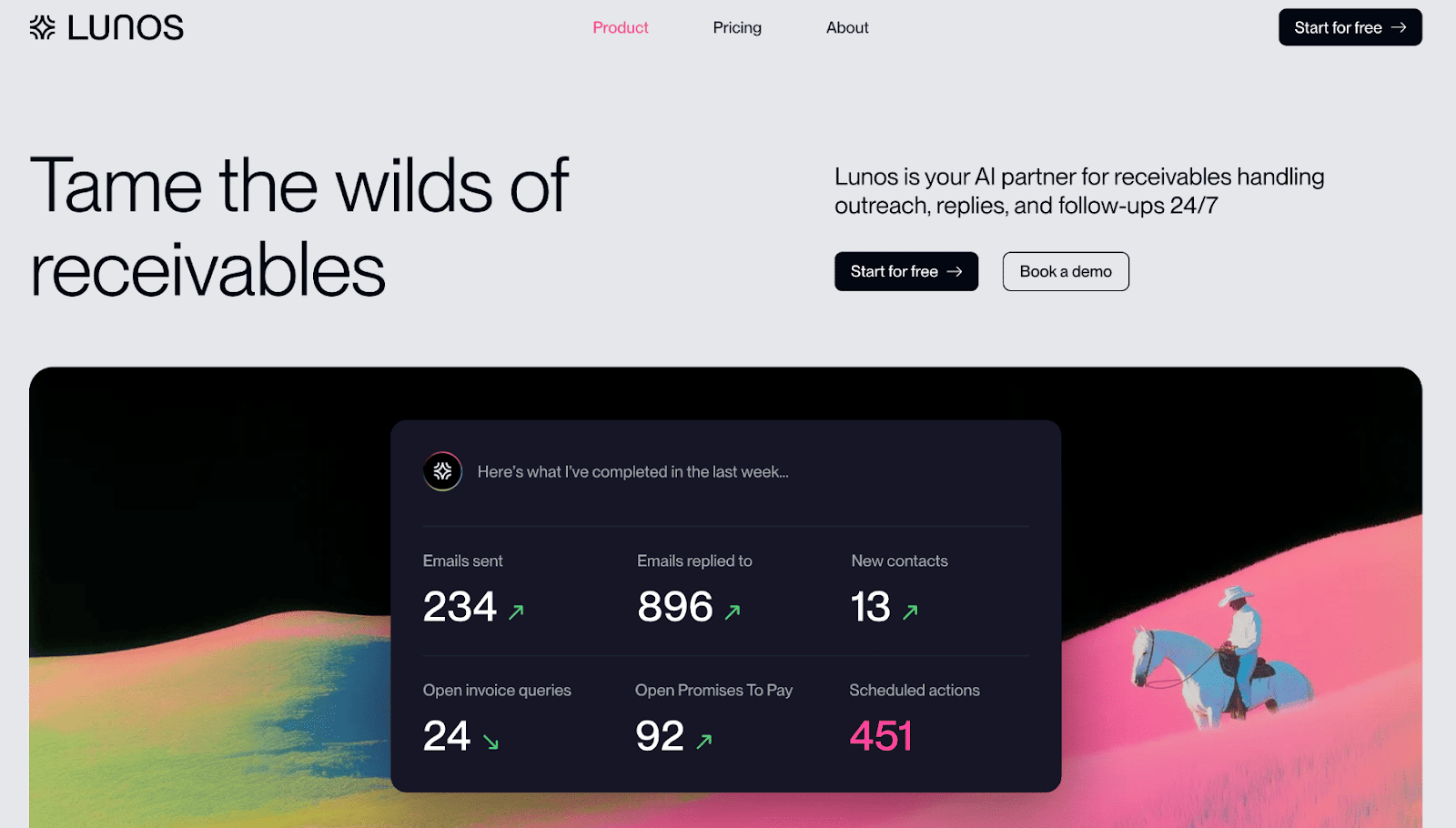

How Lunos Reduces Average Days Delinquent

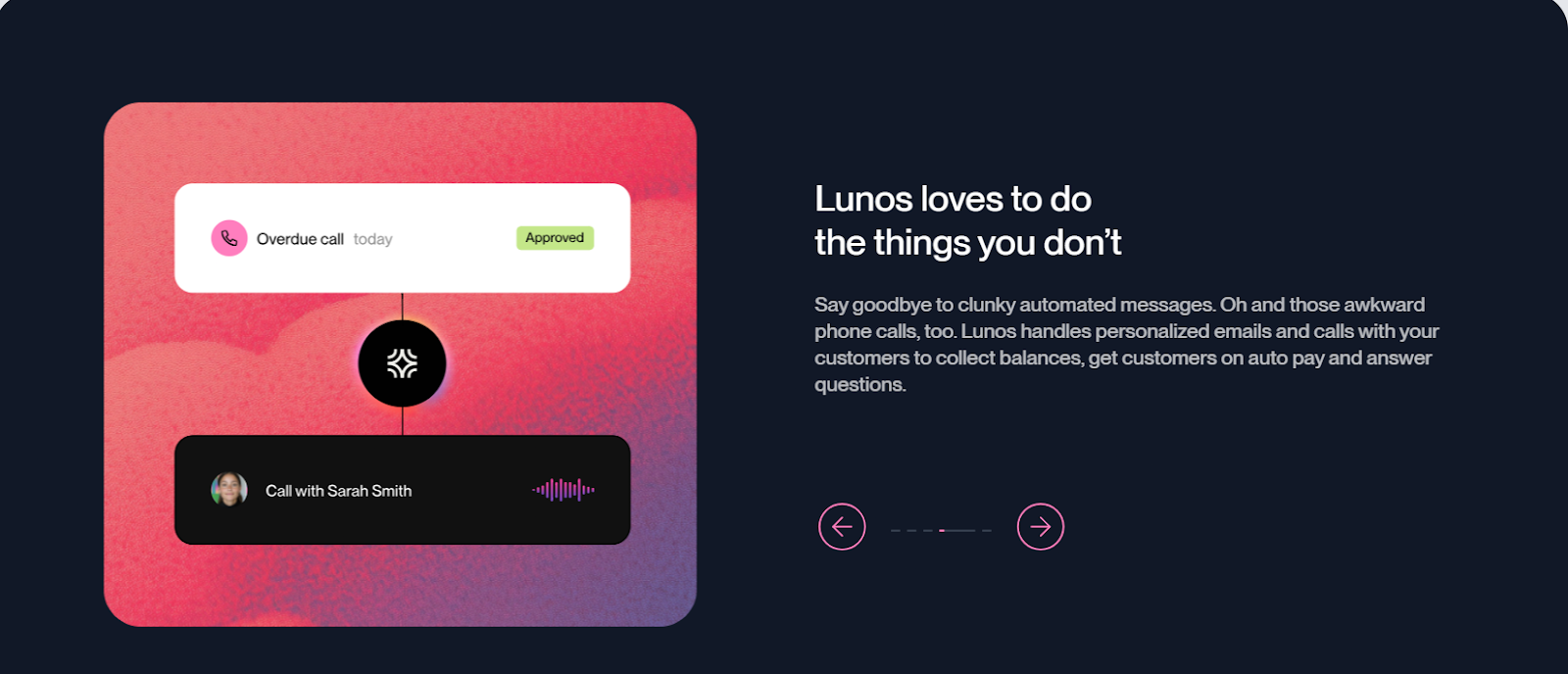

Lunos is an AI coworker for accounts receivable that handles customer follow-ups and collections like an actual human team member. While traditional AR automation sends templated reminder emails, AI accounts receivable software does what a real collector does. It reads customer responses, interprets them, and adapts its follow-up accordingly.

Here's what that looks like in practice:

Two-Way Conversational Intelligence

When a customer replies, "We'll pay this next week," Lunos doesn't just mark it as "responded." The AI recognizes this as a payment promise, schedules the appropriate follow-up for one week from now, and records the commitment for your cash forecasting. If the customer says, "I think we already paid this," Lunos recognizes it as a potential dispute and routes it to the right person on your team.

Adaptive Follow-Up that Preserves Relationships

Every customer is different. Lunos adjusts its tone, timing, and messaging based on payment history, relationship importance, and past customer responses. Your best customer, who's 5 days late, gets a friendly check-in. The chronic late payer gets a firmer reminder. Personalization happens automatically at scale.

In short, Lunos is the best dunning management software on the market thanks to its AI-powered approach.

Slack-Native Workflow that Doesn't Disrupt Your Team

Your team isn't learning a new platform or logging into yet another system. All collaboration happens right in Slack. Approve actions, review daily summaries, and step in when needed—all from where you already work.

Complete Visibility into Every Interaction

Nothing happens in a black box. Every message Lunos sends, every customer response, every payment promise. It's all tracked in real time. You get the full audit trail for compliance, and more importantly, you get accurate data for forecasting when cash is actually coming in.

Three Autonomy Modes so You Stay in Control

Start with Monitor mode, where you review everything before it goes out. Move to Suggest mode where Lunos proposes actions, and you approve them. When you're comfortable, switch to Act mode, where Lunos handles routine follow-ups automatically and flags only exceptions that require human attention.

The impact?

Teams using Lunos typically see about a 75% reduction in AR workload within weeks. That time is redirected to strategic work such as analyzing cash flow, improving processes, and handling complex situations that genuinely require human judgment.

And because Lunos is consistent, never forgets a follow-up, and adapts to customer behavior in real time, ADD drops significantly. Invoices don't sit unnoticed. Payment promises get tracked and followed up on. Disputes get surfaced immediately instead of languishing in email.

It's like having a team member who works 24/7, never gets overwhelmed, reads every single customer email, remembers every payment commitment, and knows exactly when and how to follow up with each customer. Except it's not a person. It's an AI coworker that works alongside your existing team.

Ready to see how an AI coworker can transform your collections process and bring down your ADD?

Start for free with Lunos and discover how finance teams are improving cash flow without adding headcount.

Frequently Asked Questions on Average Days Delinquent

What's the difference between ADD and DSO?

DSO measures the average time to collect from all customers. ADD focuses only on late payers, showing days past due. DSO shows overall performance; ADD reveals the true delinquency problem.

How does ADD impact my cash flow forecasting?

ADD shows how long cash is tied up in overdue invoices. The higher your ADD, the less reliable your cash flow forecasting becomes because the money you expected to receive is delayed. When you track ADD alongside payment promises and at-risk accounts (which tools like Lunos do automatically), you get much more accurate cash forecasting.

How often should I calculate ADD?

Monthly is ideal for most B2B companies. This gives you enough data to spot trends without getting lost in daily fluctuations. If you're experiencing cash flow problems or making changes to your collections process, calculate it weekly to see if your improvements are working.

Will automated reminders alone reduce my ADD?

They'll help, but they're not enough. Automated reminders ensure consistent communication, which is important. But they can't read customer responses, understand context, track payment promises, or adapt follow-ups based on customer behavior. That's why teams using AI coworkers like Lunos (which handle the actual conversations, not just send templated emails) see much bigger ADD reductions than teams using basic automation.