DSO Explained: How to Measure and Improve It

Days Sales Outstanding (DSO) measures how long it takes to collect payment after a credit sale. A lower DSO means faster cash flow, while a higher DSO means money is stuck in accounts receivable. This guide covers how to calculate DSO, what it reveals about your business, and practical ways to improve it.

Quick Summary

Days Sales Outstanding (DSO) measures how long it takes to collect payment after a credit sale. A lower DSO means faster cash flow, while a higher DSO means money is stuck in accounts receivable. This guide covers how to calculate DSO, what it reveals about your business, and practical ways to improve it.

Why DSO Matters for Your Business

Days Sales Outstanding (DSO) is one of the clearest indicators of a company's financial health. At its core, it shows how long it takes a company to collect payment after a credit sale and how efficiently a business turns sales into actual cash.

While DSO often sits with finance teams, its impact is felt across the organization. Sales teams feel it when payments arrive later than expected. Operations feel it when budgets tighten. Leadership feels it when forecasting becomes less reliable.

DSO shouldn't be treated as a back-office metric. It's an indicator that shows how smoothly a business operates and how well internal processes support cash flow.

In this article, we'll explore what DSO is, why it matters, how to calculate it, and how to improve it in practical ways.

What Is Days Sales Outstanding (DSO)?

Days Sales Outstanding (DSO) measures the average number of days between issuing an invoice and receiving payment from a customer.

It applies only to credit sales, meaning sales where customers are allowed to pay after receiving an invoice. Cash sales are excluded because payment is received immediately at the point of sale, giving them a DSO of zero days.

DSO is especially relevant for B2B companies, service providers, manufacturers, and any business operating with payment terms such as net 30 or net 60.

DSO is a key part of the cash conversion cycle (CCC), which tracks how quickly a business turns inventory and sales into usable cash. A high DSO indicates that money is tied up in accounts receivable instead of being available to run the business.

This is usually where problems start to show up, and they commonly fall into one of these scenarios:

- Cash gets tied up in unpaid invoices

- Paying suppliers becomes harder

- Growth plans slow down

- Finance teams feel the pressure fast

On the flip side, when DSO improves, the impact is often immediate. Cash flow becomes more predictable, which directly impacts how teams operate and plan.

How to Calculate DSO

The standard formula to calculate DSO is simple and straightforward:

- DSO = (Average Accounts Receivable / Net Revenue) × Number of Days

At a high level, this formula compares how much customers owe you against how much you sold during the same period.

Let's break the variables down:

Average Accounts Receivable

This is the average amount customers owe you during a specific period. Most companies calculate it by taking the accounts receivable balance at the beginning and end of the period, then averaging the two.

Net Revenue

Net revenue is your total sales after subtracting returns, refunds, and discounts for the same period.

Number of Days

This is usually 365 for annual calculations, or the number of days in the specific period you're analyzing.

A Simple DSO Example

As a practical example, let's say a B2B services company reports the following figures for the year:

- Beginning accounts receivable: €900,000

- Ending accounts receivable: €1,100,000

- Net revenue: €6,000,000

First, calculate the average accounts receivable:

(€900,000 + €1,100,000) / 2 = €1,000,000

Now apply the formula:

DSO = (€1,000,000 / €6,000,000) × 365

DSO = 61 days

In a real-life scenario, this means the company waits about two months, on average, to get paid.

If the company's payment terms are net 30, this gap becomes significant. On paper, customers should be paying within 30 days. That difference is exactly what affects cash flow.

The "Count Back" (or Roll-Back) Method

For companies with seasonal or uneven sales, the standard formula may not tell the full story. In these cases, the count-back method offers a more realistic view.

This approach starts with the total outstanding receivables and subtracts monthly sales one period at a time until the balance is cleared. It shows which months' sales are still unpaid.

This method mirrors real payment behavior and works particularly well for month-by-month tracking. The downside is that it requires more frequent updates and more detailed data, which can be harder and time-consuming to manage manually.

What DSO Actually Tells You

DSO speaks volumes about how money moves through the business. It reflects how well invoicing, collections, and customer payment behavior are working together.

For example, consider these two scenarios:

When DSO Is High

A high DSO usually points to friction somewhere in the process, such as:

- Customers are paying late

- Invoices aren't going out on time

- Disputes aren't being resolved quickly

- Credit terms are too generous

- No one really owns collections

When DSO Is Low

A lower DSO suggests things are working as they should. It reveals how aligned different teams are internally. In many organizations, payment terms are negotiated by sales while invoices are issued by finance. When these areas aren't aligned, delays become more likely. A low DSO shows well-defined responsibilities and teams working toward the same expectations.

Why Tracking DSO Over Time Is Important

A single DSO number only shows a snapshot in time. On its own, it doesn't tell much. The real value comes from tracking DSO over time, which allows you to spot patterns like:

- Is DSO slowly creeping up each quarter?

- Does it spike during certain seasons or busy periods?

Some fluctuation is normal, especially for seasonal businesses. What usually signals a problem is consistent upward movement or sudden, unexplained changes. That's why financial teams track DSO to keep warning signs in check.

What Is Considered a Good DSO?

There's no universal benchmark for what constitutes a good DSO. However, many companies aim for a DSO under 45 days. The best approach is to compare your DSO against benchmarks for different industries.

Keep in mind that what's considered "good" depends heavily on the industry and business model.

For example:

- Software and professional services often sit around 30-40 days

- Manufacturing and construction usually run higher, often exceeding the 40-day mark

- Retail and transactional businesses tend to be much lower (0-5 days)

In short:

The most useful comparisons usually involve:

- Your own historical performance

- Industry peers with similar customers and deal sizes

It's also important to factor in business maturity. Early-stage companies may accept longer payment cycles to win customers and build relationships. More established businesses often focus on tightening terms and improving predictability.

Geography can play a role as well. Payment behavior varies by market, and what's considered normal in one region may feel slow in another.

Common Reasons Why DSO Starts Increasing

When DSO rises, it's rarely due to one big problem. More often, it's the result of small operational gaps adding up over time.

Common causes include:

- Invoices are sent late after delivery or project completion

- Errors that delay approval or payment

- Customers prioritizing other suppliers

- Payment terms that aren't enforced consistently

- Sales teams extending terms to close deals

- Disputes that remain unresolved for too long

Individually, these issues don't always feel critical, which is why DSO can worsen if it isn't monitored closely.

Another common factor is growth. When sales increase quickly, invoicing and collections processes don't always scale at the same pace. What worked for a smaller customer base may struggle under high volume.

This is often when manual processes start to break down. Invoices get delayed, reminders aren't sent on time, and visibility into overdue balances decreases.

How to Improve DSO

Reducing DSO improves liquidity and lowers the pressure on day-to-day cash flow. In practice, it also reduces the need for short-term financing and gives finance teams more control.

DSO usually improves when several small things are done consistently.

Below are proven techniques that help businesses reduce DSO and accelerate cash collection:

1. Automate and Accelerate Your Invoicing Process

Good invoicing is the foundation of healthy cash flow, but speed and consistency matter just as much as accuracy. The faster invoices reach customers after delivery, the faster payment cycles begin.

Key strategies include:

- Automate invoice generation immediately after delivery or service completion

- Set up recurring invoices for subscription or retainer-based work

- Use invoice templates that include all required information upfront to avoid back-and-forth

- Integrate your invoicing system with your CRM and accounting software to eliminate manual data entry

- Include direct payment links to reduce friction

Every day of delay between delivery and invoicing adds directly to DSO. Companies that automate this step often see immediate improvements because customers receive invoices while the value is still fresh in their minds.

Common invoicing mistakes like incorrect amounts, missing purchase order numbers, or unclear payment instructions give customers an easy excuse to delay payment. When invoices require clarification or correction, the payment clock effectively resets.

2. Assess Credit Risk Before Extending Terms

Before offering payment terms, understand who you're dealing with. Not all customers deserve the same terms.

For new customers, conduct basic credit checks. This might include reviewing company financials, checking credit reports, or requiring references from other suppliers. The goal isn't to block sales, but to avoid extending generous terms to customers who represent high payment risk.

For existing customers, let payment history guide your decisions. If a customer consistently pays 60 days on net 30 terms, consider:

- Requiring partial payment upfront

- Shortening payment terms to net 15

- Offering early payment discounts to incentivize faster settlement

- Moving high-risk accounts to a more aggressive follow-up schedule

3. Create a Structured Follow-Up Process

No overdue invoice should slip through the cracks. The difference between companies with low DSO and high DSO often comes down to follow-up consistency.

An effective follow-up cadence typically includes:

- Day -3: Friendly reminder before the due date

- Day 0: Invoice due date confirmation

- Day +7: First follow-up for overdue invoices

- Day +14: Second follow-up with more urgency

- Day +30: Escalation to senior contact or collections team

Personalized messages work better than generic templates. Reference specific invoice numbers, amounts, and due dates. Include direct payment links. Acknowledge the relationship while being clear about expectations.

Manual collections don't scale.

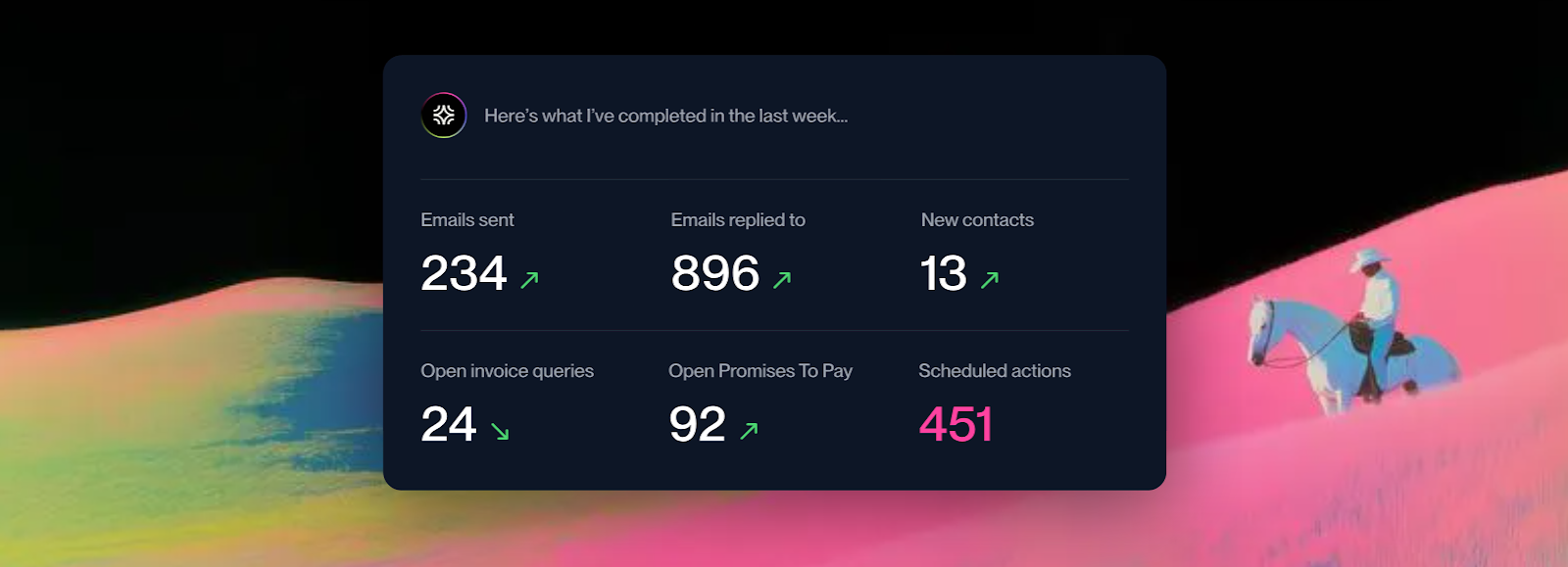

As invoice volume grows, spreadsheets break down, reminders get missed, and visibility disappears. This is where AI in accounts receivable makes a measurable difference. Tools like Lunos automate the entire collections workflow, from initial outreach to follow-ups and customer replies.

It reads customer responses, understands payment promises, identifies disputes, and adapts follow-ups based on context. Teams that implement automated collections typically see DSO improvements within weeks.

4. Make Payment Effortless

The easier you make it for customers to pay, the faster you'll get paid.

Offer multiple payment options including bank transfer, credit card, ACH, and digital wallets. Different customers have different preferences and internal processes. Providing options removes friction.

Beyond payment methods, consider:

- Including direct payment links in every invoice and reminder

- Setting up customer payment portals where they can view all outstanding invoices

- Offering automated payment plans for large balances

- Providing early payment discounts (1-2% for payment within 10 days can significantly accelerate cash collection)

Payment options should be prominently displayed in every customer communication, not buried in fine print.

5. Align Sales and Finance on Payment Terms

DSO problems often start during the sales process. When sales teams extend overly generous payment terms to close deals, they're creating future cash flow problems for the finance team.

Create clear guidelines around:

- Standard payment terms by customer type

- Who has authority to approve exceptions

- How payment terms impact commission or deal approval

- The real cost of extending terms (delayed cash, increased risk)

When sales and finance work from the same playbook, customers receive consistent expectations and payment terms become easier to enforce.

Final Thoughts

Days Sales Outstanding reveals how efficiently your business converts credit sales into cash. While the calculation is straightforward, the real challenge lies in managing it consistently.

A high DSO isn't just a finance problem. It affects your ability to invest in growth, pay suppliers on time, and maintain financial flexibility. The good news is that DSO improves when you focus on the fundamentals: accurate invoicing, structured follow-ups, and smart automation.

The companies that maintain healthy DSO aren't necessarily the ones with the easiest customers. They're the ones with better processes.

Ready to reduce your DSO and improve cash flow? Start for free with Lunos AI and see how an AI coworker can handle your receivables at scale, reduce collection time by weeks, and free your finance team to focus on strategy instead of chasing payments.