11 Best Payment Orchestration Software Tools for 2026

Quick Summary

Payment orchestration software sits above your processors and gateways as a single control layer, letting you route transactions, manage failovers, and add new payment methods without rebuilding integrations from scratch.

Here are our top picks:

Why Payment Orchestration Software Matters

Adding a new payment provider should be easy. In reality, it rarely is.

Each provider comes with its own integration, reporting format, and operational quirks. What starts as a simple improvement to approval rates often turns into a growing web of APIs, dashboards, and payment rules that teams must maintain.

Over time, this creates a hidden operational burden. Engineering teams spend more time maintaining payment infrastructure, while finance teams struggle to get a clear view of how payments are performing across processors and regions.

Payment orchestration software solves this by sitting above your providers as a control layer. In this article, we break down the 11 best payment orchestration platforms for 2026, highlighting each one's key features, pros, cons, and pricing.

Why Listen to Us?

Lunos works with finance teams handling 500 to 50,000 invoices per month.

Backed by General Catalyst and Cherry Ventures, we've built AI that reduces manual AR workload by 75% by handling the communication and negotiation that holds up cash application.

11 Best Payment Orchestration Software: A Quick Comparison

1. Lunos

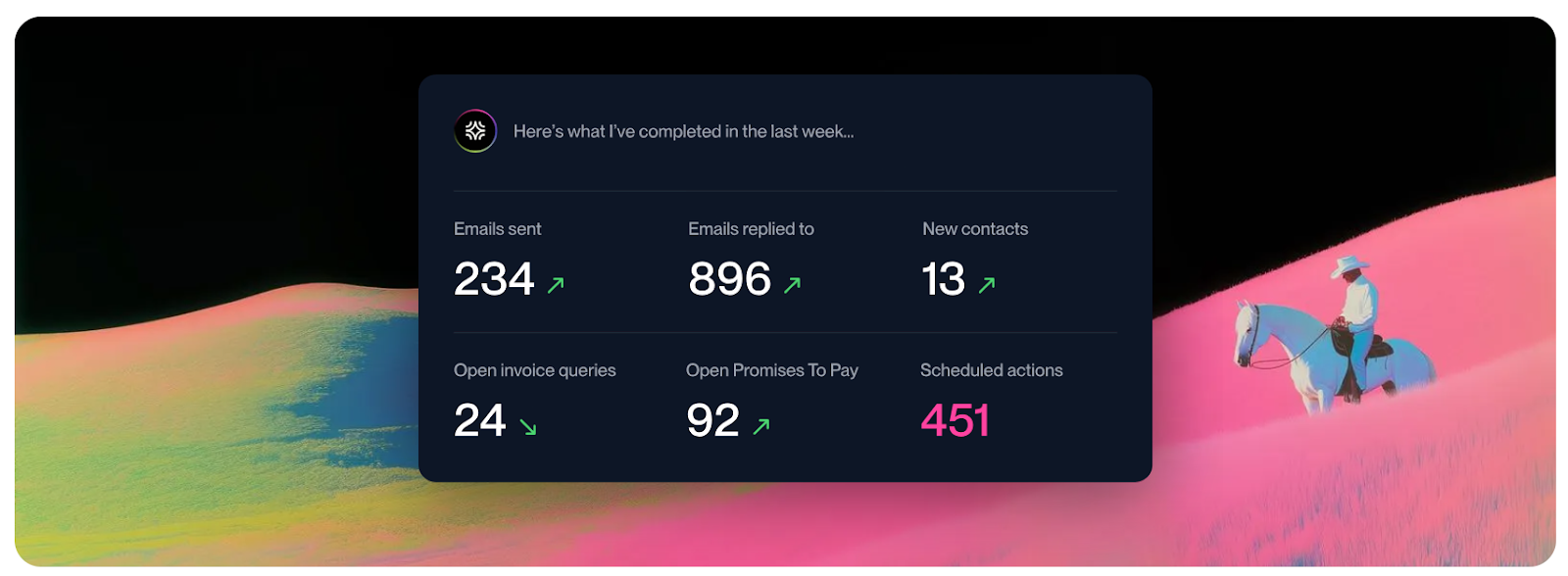

Lunos acts as an autonomous coworker for your finance team, orchestrating your ERP, CRM, and email into a single workflow. Instead of sending one-way reminders, it reads and understands customer email replies to identify their intent and handle the follow-up.

Lunos recognizes when a customer asks for an extension or raises a billing dispute, then either handles the routine response or flags it in Slack. This allows your team to scale collection efforts and manage a higher volume of invoices without adding headcount.

Key Features

- Reads and understands customer email replies to manage the back-and-forth communication required to close an invoice.

- Provides Monitor, Suggest, and Act modes to control the level of independence the system has in your payment collection strategy.

- Connects NetSuite, QuickBooks, Xero, and Salesforce to ensure your payment records and customer communications are perfectly aligned.

- Operates entirely within Slack, so you can organize your daily collection tasks and approve AI actions without switching apps.

- Automatically identifies and routes complex payment disputes or specific customer questions to the right person on your team.

- Learns from customer behavior to adjust the tone and timing of every message for better collection results.

Pricing

- Starter: $0/month (0.3% fee on collected revenue).

- Pro: $200/month + 0.3% fee.

- Enterprise: Custom pricing.

Pros

- Your team can cut the manual AR workload by about 75%, moving away from admin tasks toward higher-level strategy.

- Consistent, intelligent follow-ups mean invoices get paid sooner, directly lowering your DSO within the first few weeks.

- Customers receive friendly, personalized notes that feel like they came from a person, not a rigid "no-reply" bot.

- Because Lunos tracks actual payment commitments from emails, your cash flow projections become much more accurate.

Cons

- The platform is built for relationship-based invoicing, so it’s not a fit for simple, "buy now" checkouts.

- Pricing not available upfront.

2. Primer

Primer is a unified payment infrastructure that lets you build and manage your entire payment stack through one interface. It's a no-code canvas for businesses that want to connect different processors, fraud tools, and payout methods without writing new code for every update.

Key Features

- Drag-and-drop canvas to build and update your payment logic without needing engineers

- Compliant vault to securely manage and move payment credentials between different providers

- Unified dashboard that tracks all your payment data and monitors performance in real-time

Pricing

- Quote-based.

Pros

- You don’t have to write custom code every time you want to add a new payment method

- Helps recover lost revenue by instantly retrying failed payments through alternative routes

- Makes global reporting much easier by putting all your data in one standardized view

Cons

- Only handles the checkout moment, not the long-tail communication of B2B collections

- You’ll still need someone who understands payment strategy to map out complex global flows

- Lacks the conversational intelligence needed to handle customer replies or specific billing disputes

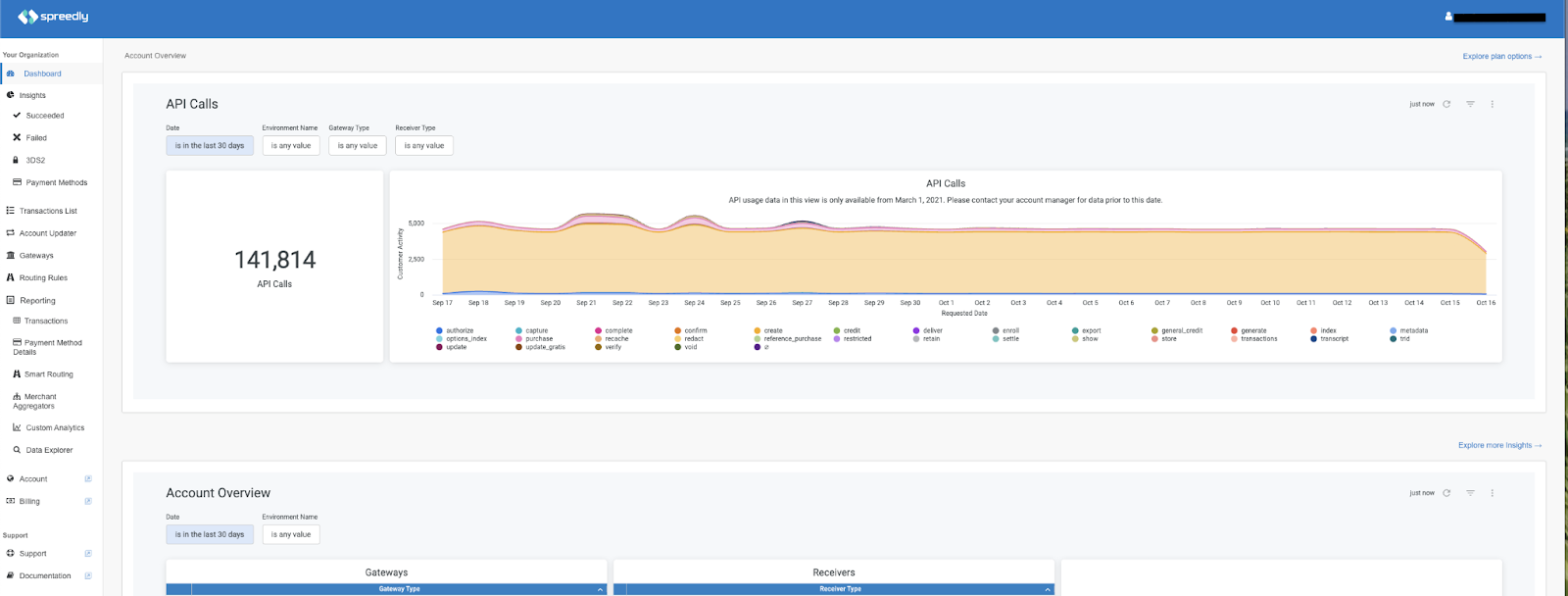

3. Spreedly

Spreedly is a cloud-based payments orchestration platform that helps you build a flexible, global payment stack. It sits between your business and various payment service providers, offering the infrastructure to route transactions and vault data without being locked into a single processor.

Key Features

- Independent PCI-compliant vault that lets you store and move card data between 120+ different gateways

- Single API to connect with a global network of payment gateways, fraud tools, and 3-D secure services

- Network tokenization and card lifecycle management to automatically update expired or replaced cards

- Support for regional compliance requirements like PSD2 and 3DS2 across multiple markets

Pricing

- Custom, quote-based pricing.

Pros

- Prevents gateway lock-in by ensuring you own and keep control over your customer payment data

- Simplifies the technical side of global security and PCI compliance

- Provides redundancy by allowing you to switch gateways instantly if one goes down

Cons

- Not a payment processor, so you still have to manage individual relationships with your PSPs

- Highly technical and usually requires developer resources to set up and maintain

4. Gr4vy

Gr4vy is a cloud-native orchestration platform that simplifies how businesses scale and manage global payments. It offers an "Infrastructure as a Service" (IaaS) model, giving you a dedicated cloud to deploy new payment methods, manage fraud, and route transactions across providers.

Key Features

- No-code rules engine that allows you to create dynamic payment filters and workflows from a central dashboard

- Dedicated cloud-native vault to centralize your card data and network tokens while ensuring data portability

- Smart routing logic that automatically selects the most cost-effective or highest-performing route for every transaction

- Integrated Sandbox environment for testing new payment strategies and configurations before they go live

Pricing

- Quote-based model.

Pros

- Fast to deploy new payment methods or change your routing strategy

- The dedicated cloud instance provides better resilience and redundancy than shared orchestration environments

Cons

- While no-code, the sheer number of options (400+ integrations) can be overwhelming for smaller finance teams

- Requires an existing checkout flow or app to connect to, as it doesn't offer a standalone billing portal

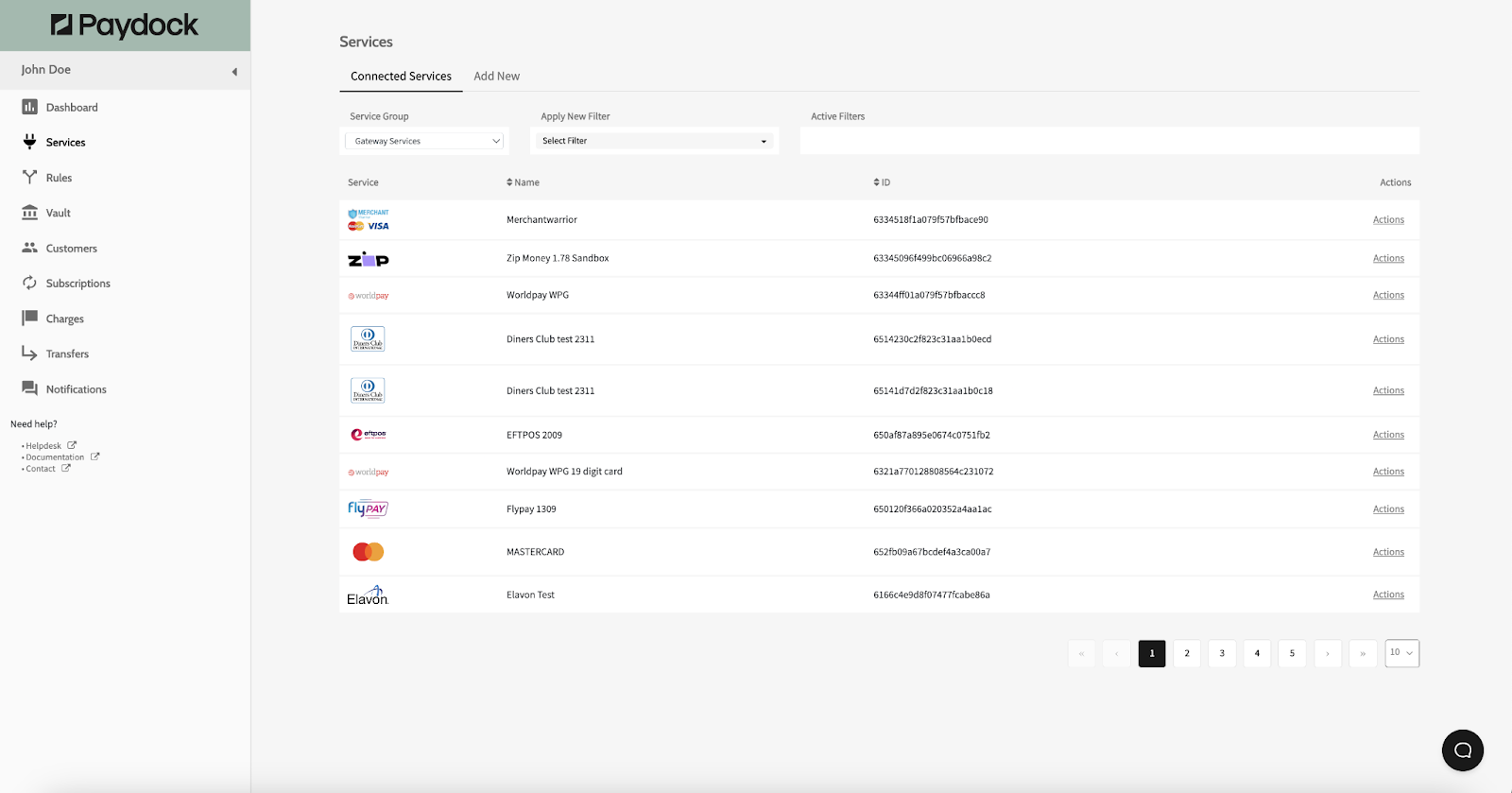

5. Paydock

Paydock is an enterprise-grade orchestration platform designed to simplify the management of multiple payment providers. It acts as a single point of control for your entire payment ecosystem, consolidating banks, gateways, and local payment methods into a unified flow.

Key Features

- Single API that connects multiple payment gateways, processors, and payment services

- A dynamic payment routing engine that directs transactions based on rules like currency, network, or geography

- Secure token vault that stores payment data and allows transactions across multiple providers

- Support for adding global and alternative payment methods without complex integrations

Pricing

- Quote-based model.

Pros

- Reduces the administrative headache of managing separate vendor relationships and disparate reporting

- Lower your overall transaction costs by routing payments to the most cost-effective provider available

- Offers great flexibility for businesses operating in multiple regions that need diverse, localized payment options

Cons

- The platform's depth is designed for high-volume operations and may be overkill for smaller startups

- Requires an initial technical lift to integrate the API or widget into your current financial systems

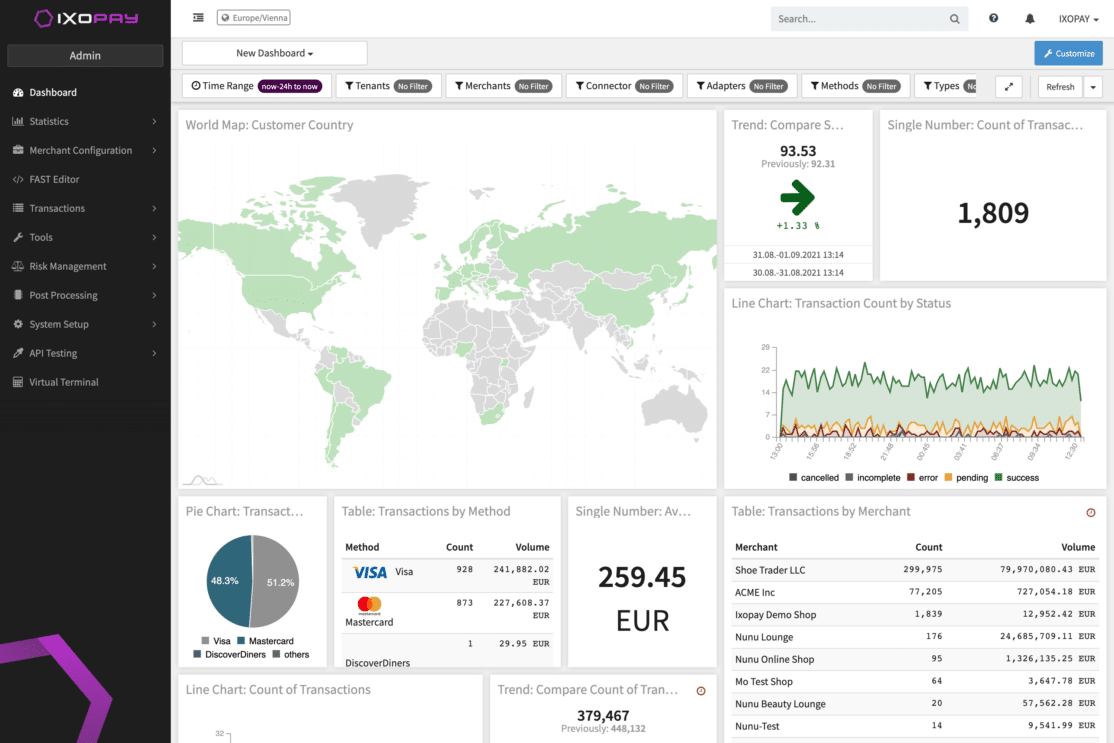

6. IXOPAY

IXOPAY is a highly scalable payment orchestration platform built for global enterprise merchants. It acts as a neutral, provider-agnostic layer that centralizes everything from transaction routing to risk management.

Key Features

- PCI-compliant card vault that tokenizes and securely stores payment data across providers

- Post-processing engine that automates reconciliation and settlement across PSP formats

- Risk management engine that allows you to set unified fraud prevention rules across your entire payment stack

- Fee management engine that calculates external commissions in real-time to provide an instant view of processing costs

Pricing

- Custom enterprise pricing.

Pros

- Provides complete independence from processors, letting you swap or add gateways with zero downtime

- Reduces accounting overhead by consolidating fragmented data into a uniform reporting format

- Helps recover revenue through automated fallback routing if a preferred provider goes offline

Cons

- It may be too complex for smaller teams to manage effectively

- Requires a technical integration period to connect the API with your existing CRM and ERP systems

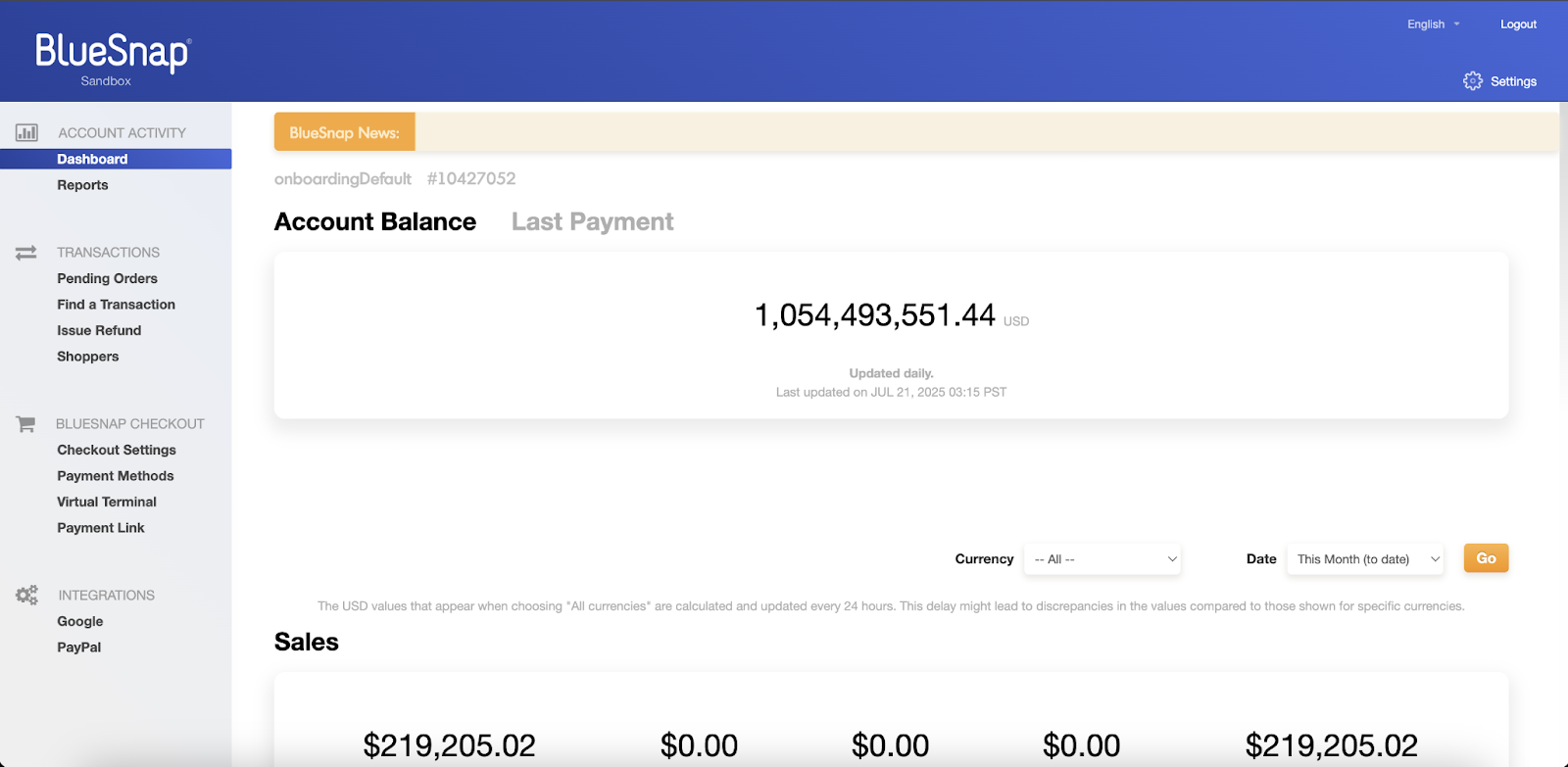

7. BlueSnap

BlueSnap positions itself as an "All-in-One" Payment Orchestration Platform. Unlike pure orchestrators that just sit on top of other banks, BlueSnap is a licensed processor with orchestration built in.

This means you get the smart routing and failover of an orchestrator, but with a single contract and account. This significantly reduces the vendor fatigue of managing a dozen different relationships.

Key Features

- Automatically routes transactions to local banks to avoid cross-border fees and boost authorization rates.

- Includes tools for automated invoicing and invoice-to-cash workflows.

- Easily activate fraud prevention, tax calculations, and chargeback management by region.

- One set of reports for all global sales channels, including online, mobile, and manual phone orders via virtual terminal.

Pricing

- Custom-based pricing.

Pros

- You get the benefits of a global multi-bank strategy without having to sign and manage multiple individual PSP contracts.

- Handles Level 2 and Level 3 data processing, which lowers costs for high-value B2B transactions.

- Automated dunning process for failed recurring payments.

Cons

- The merchant control panel can be a bit dense and technical compared to newer, no-code competitors.

- Some mid-market users have reported slower response times during complex technical setups.

8. Akurateco

Akurateco is a white-label orchestration platform that unifies hundreds of gateways and banks through a single API. It acts as a central hub for enterprise merchants and payment providers to manage global transaction routing and provider independence.

Key Features

- Access to over 600 integrations with global banks and alternative payment methods through one connection

- An intelligent routing engine that directs transactions based on fees and geography to ensure high success rates

- Built-in cascading feature that automatically retries declined payments through backup providers in real-time

- Risk engine with over 150 customizable fraud filters and risk-scoring modules

- Consolidated reporting that unifies transaction data from all connected providers into one dashboard

Pricing

- Quote-based

Pros

- Typically increases approval rates through its smart routing and cascading engines

- Allows for a fast time-to-market by enabling companies to launch a branded platform

- Helps businesses significantly reduce cross-border processing fees by routing to local acquirers

- On-premise deployment options are available for companies needing total control over data infrastructure

Cons

- Managing 150+ fraud filters and complex routing rules often requires a specialized payment manager

- Focuses on transaction uptime and technical health rather than manual accounts receivable follow-up tasks

9. Solidgate

Solidgate provides payment orchestration and infrastructure for global companies, with a strong focus on subscription models and high-growth digital businesses. It unifies multiple processors and payment methods into a single dashboard, so you don't have to build your own stack from scratch.

Key Features

- No-code payment links that you can send via email or chat to collect payments without a website

- Customizable payment forms that embed directly into your site for a seamless checkout experience

- Intelligent routing and failover that sends transactions to the bank

- An independent token vault that keeps card data portable even if you change processors or banks

Pricing

Custom, quote-based pricing

Pros

- Capture more revenue by automatically recovering failed transactions through smart routing

- Speeds up expansion into new markets by providing instant access to local acquiring

- Reduces manual back-office work by automatically reconciling payments across your entire global stack

- Strong technical reliability, high uptime guarantee, and multi-region infrastructure

Cons

- Does not handle human-led collection conversations or email follow-ups

- Setting up complex routing rules and anti-fraud filters usually requires a dedicated person to manage them

10. PayU

PayU offers a global payment orchestration platform specifically designed for large enterprises expanding into high-growth markets. It unifies local and international payment methods through a single API, focusing on markets like Latin America, Africa, and Central/Eastern Europe.

Key Features

- Single API that connects multiple payment providers and online payment methods

- Smart routing engine that directs transactions through the most optimal processing path

- Universal token vault that stores payment tokens across providers

- Built-in payment security and anti-fraud tools

Pricing

Quote-based pricing.

Pros

- Supports cross-border payments with many global and local payment methods

- Smart routing helps improve approval rates and reduce payment failures

- Single integration simplifies global payment infrastructure

- Provides centralized analytics and reporting for payment performance

- Includes built-in fraud protection and compliance features

Cons

- Primarily designed for ecommerce and online payment processing

- Implementation may require technical payment infrastructure knowledge

- Focuses on transaction routing rather than invoice-based payment workflows

11. Yuno

Yuno is a payment orchestration platform that helps businesses connect multiple payment providers and payment methods through a single integration.

It is designed for companies operating globally that want to manage payments, routing, and performance across different markets without building a complex payment infrastructure.

Key Features

- Connects multiple payment providers and gateways through a single API

- Smart routing that directs transactions to the processor most likely to approve them

- Access to hundreds of global and local payment methods

- Fraud prevention integrations and payment risk controls

- Tools for managing payment analytics and provider performance

Pricing

- Custom pricing.

Pros

- Supports many global payment providers and payment methods

- Single integration simplifies complex payment infrastructure

- Smart routing helps reduce failed transactions

- Centralized dashboards improve visibility into payment performance

Cons

- The platform’s 1,000+ integrations are geared toward enterprise scale and may be overkill for smaller merchants

- Managing the advanced routing logic and fraud rules requires a dedicated payment or operations lead

Why Payment Orchestration Platforms Often Fall Short for B2B Payments

While traditional payment orchestration platforms are excellent at the technical plumbing of a transaction, they are often built for high-volume B2C ecommerce where a customer either pays at checkout or doesn't. In B2B, the transaction is only a small part of the story.

Here’s why:

The "Silent" Gap

Standard orchestrators focus on routing a payment once it’s initiated. However, they don't help you get the customer to initiate that payment in the first place. They are blind to the weeks of emails, PDF attachments, and "checks in the mail" excuses that define B2B cycles.

Lack of Context

A technical orchestrator doesn't know why a customer hasn't paid. It can’t distinguish between a technical bank decline (which it can fix with smart routing) and a customer who hasn't paid because they have a question about a line item on their invoice.

Rigid Checkout Flows

Most orchestration tools are designed for a "Buy Now" button. B2B payments often require negotiation, partial payments, or specific net terms that don't fit within standard ecommerce checkout logic.

Data Silos

While they consolidate transaction data, they rarely sync with your CRM or communication history. This leaves your finance team jumping between a payment dashboard and their email inbox to understand the true status of an account.

How Lunos Solves B2B Payment Orchestration Challenges

Lunos moves beyond the technical switch by treating B2B payments as a communication problem, not just a routing problem. It bridges the gap between your payment rails and your customer relationships.

Here’s how:

Relationship-Aware Collections

Unlike traditional orchestrators that only trigger after a click, Lunos uses AI to manage the pre-payment phase. It handles the outreach, adapts to your customer’s tone, and answers questions, ensuring the payment actually gets started.

Dynamic B2B Workflows

Lunos handles the messy reality of B2B. This includes supporting complex net-terms, automated follow-ups, and the human back-and-forth required to move money between businesses.

Unified Conversation & Payment Data

Lunos consolidates your accounts receivable data with your customer interactions. You get a single view of where the money is and what was said to get it there. This integrates directly with your ERP and CRM.

B2B-First Optimization

While Lunos still provides the efficiency of a unified payment layer, the orchestration focuses on the entire lifecycle, from the moment an invoice is sent to the moment the cash is reconciled in your books.

Solving the B2B Payment Gap

Most payment orchestration platforms focus on routing transactions at checkout.

But B2B payments rarely work that way. Invoices, payment promises, and follow-ups still create manual work for finance teams.

If your real challenge is collecting payments after the invoice is sent, Lunos helps automate those conversations and keep collections moving.

Ready to automate the outreach behind your payments?

Get started with Lunos today.